The Simplest Idea in Investing (That Most People Ignore)

Imagine you are watching two runners in a race. One has been leading for the last few laps and gaining speed. The other has been falling behind and losing energy. If you had to bet on who would be ahead at the next checkpoint, who would you pick?

Most people would bet on the leader. In investing, this intuition turns out to be quite profitable.

This is the essence of momentum investing: assets that have been rising tend to keep rising, and assets that have been falling tend to keep falling. It sounds almost too simple to be true. However, decades of research, starting with professors Narasimhan Jegadeesh and Sheridan Titman in 1993, have shown that momentum is one of the most reliable patterns in financial markets.

What Exactly Is Momentum?

In physics, momentum refers to the tendency of a moving object to stay in motion. In finance, the idea is similar.

When we discuss investment momentum, we mean this: if a stock, ETF, or entire market has performed well over the past several months (typically 6 to 12 months), it is statistically more likely to continue performing well in the near future. The same holds true for underperformers; they tend to keep underperforming.

Jegadeesh and Titman demonstrated this concept in their influential 1993 study. They analyzed decades of US stock data and found that buying recent winners and avoiding recent losers led to significant extra returns, even after considering risk. The effect was so strong that even Eugene Fama, known for the "efficient market hypothesis" (which suggests markets are impossible to consistently beat), referred to momentum as the top anomaly his models could not explain.

Why Does Momentum Work? (The Human Factor)

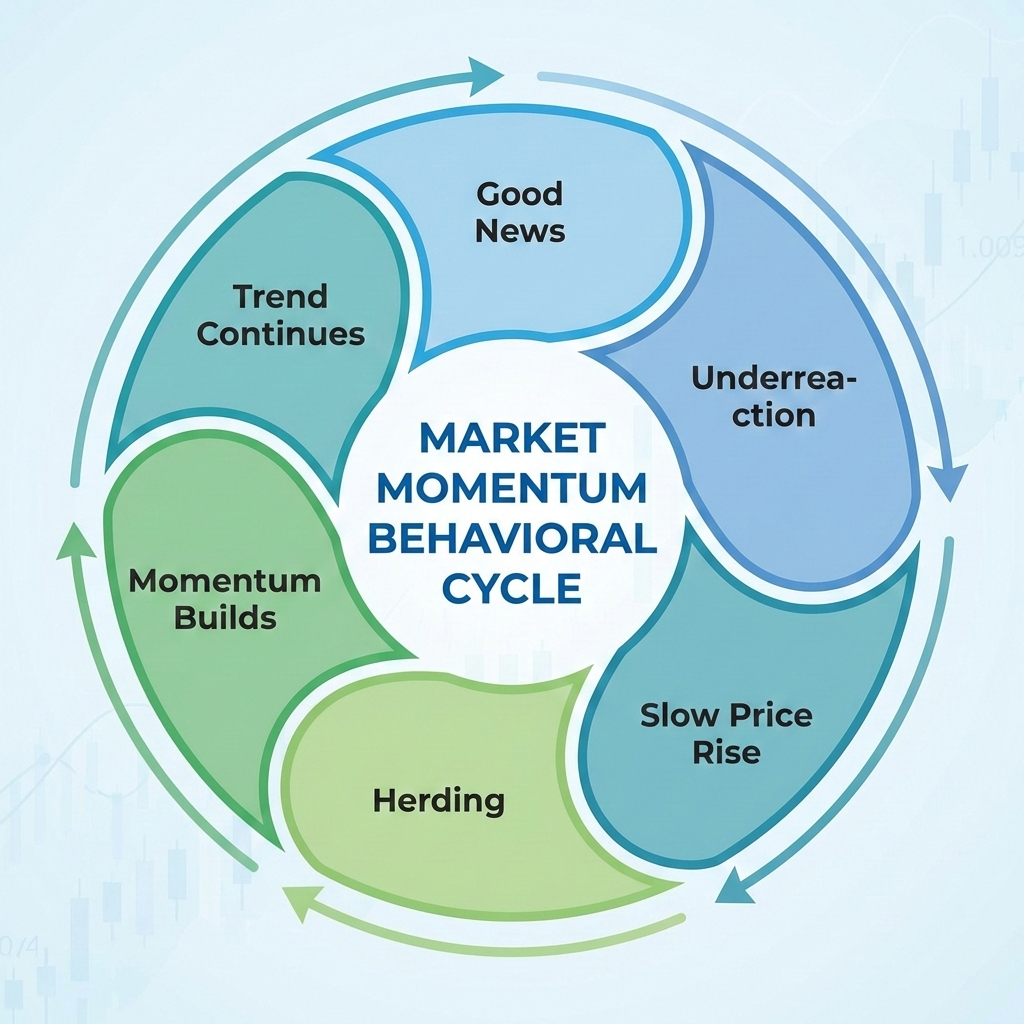

If momentum is such a reliable pattern, why doesn't everyone take advantage of it until it disappears? The answer lies in human psychology.

Research from behavioral finance, a field pioneered by Nobel laureate Daniel Kahneman and his colleague Amos Tversky, shows that investors are not the rational decision-makers traditional economics assumes. We are emotional, biased, and often predictably irrational. Three key biases drive momentum:

1. Underreaction to news

When a company reports great earnings or a sector shows strength, investors often update their expectations slowly. They cling to old prices and beliefs. Researchers Harrison Hong and Jeremy Stein found in 1999 that information spreads gradually among investors; not everyone gets the updates at the same time. This slow adjustment means prices take time to reach their fair value, creating a trend that momentum investors can follow.

2. Herding behavior

As an asset rises, more investors notice and jump in. Media coverage increases, and friends talk about it at dinner parties. This creates a cycle where buying leads to more buying. Robert Shiller documented this pattern extensively in his book Irrational Exuberance. Rising prices create stories that attract more buyers, pushing prices even higher.

3. The disposition effect

Kahneman and Tversky found that people feel the pain of a loss roughly twice as strongly as the pleasure of an equivalent gain. This means investors tend to sell their winners too early (locking in gains feels good) while holding onto their losers too long (selling at a loss feels painful). This behavior slows price movements, allowing momentum strategies to profit from the delay.

The Evidence: How Strong Is Momentum?

The academic evidence for momentum is extensive and covers multiple markets and time periods:

- It works across asset classes: stocks, bonds, commodities, currencies, and real estate (Asness, Moskowitz, and Pedersen, 2013).

- It works across geographies: tested and confirmed in over 40 countries (Rouwenhorst, 1998).

- It works across time: documented in data spanning over 200 years (Geczy and Samonov, 2016).

- It has withstood academic scrutiny: over 300 published papers confirm the effect.

Cliff Asness, founder of AQR Capital Management (one of the world's largest quantitative investment firms), co-authored a landmark 2014 paper titled "Fact, Fiction and Momentum Investing," which systematically addressed common objections to momentum. The paper showed that momentum is not just a statistical anomaly; it is not negated by trading costs, and it is not confined to small or illiquid stocks.

Momentum Investing vs. Buy-and-Hold

You might be thinking: "I already invest in index funds. Isn't that good enough?"

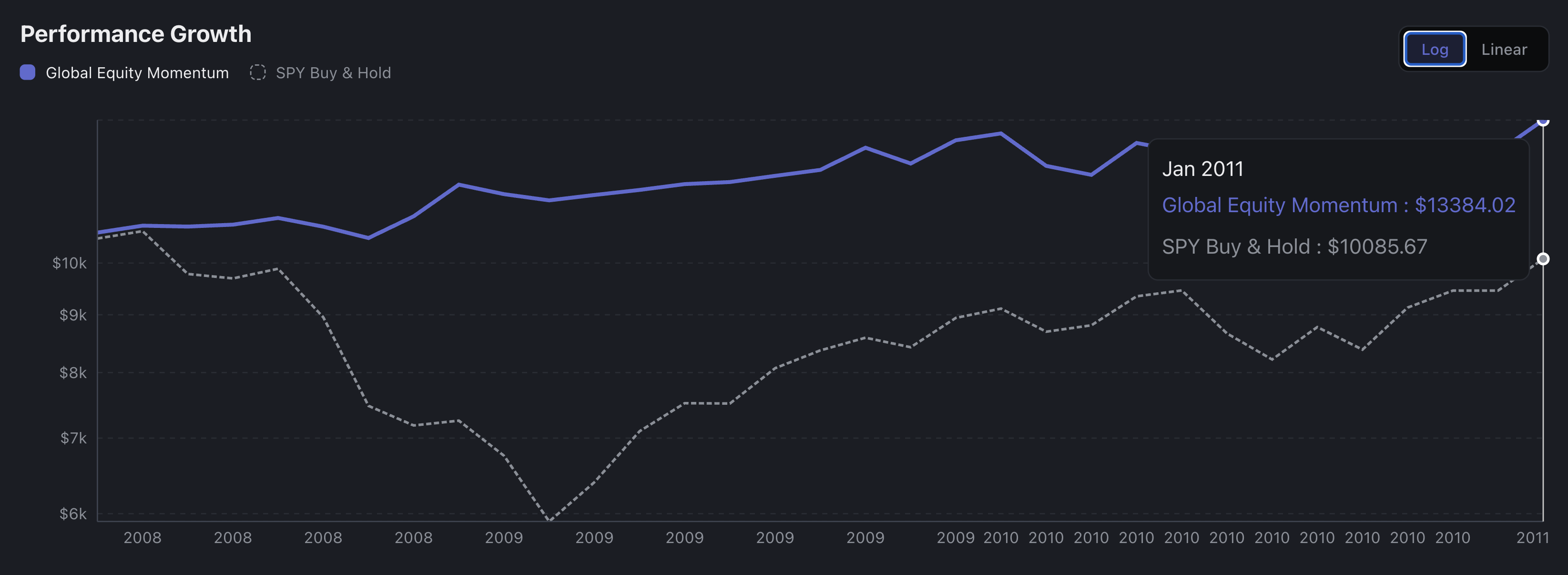

Index fund investing (buy-and-hold) is a great starting point. It's simple, low-cost, and outperforms most active fund managers. However, it has a significant weakness: it offers no downside protection. During the 2008 financial crisis, the S&P 500 dropped 55%. During the 2000-2002 dot-com crash, it fell 49%. You had to endure those losses and hope for recovery.

Momentum strategies add an essential layer: they can detect when the market is weakening and shift to safer assets (like bonds or cash) before the worst of a crash occurs. Think of it as buy-and-hold with a safety belt.

Two Types of Momentum (A Quick Preview)

Not all momentum is the same. Researchers have identified two distinct types, and the most effective strategies combine both:

Absolute momentum (also called "time-series momentum"): Is this asset going up or down compared to a safe alternative? If stocks have performed better than Treasury bills over the past 12 months, the trend is positive, so stay invested. If not, move to safety. Think of it as asking: "Should I be in the market at all right now?"

Relative momentum (also called "cross-sectional momentum"): Among the assets that are trending up, which one is gaining the most? If US stocks are outpacing international stocks, lean towards US stocks. Think of it as asking: "Given that I should be invested, where should I put my money?"

Gary Antonacci, a seasoned investment professional, combined these two types into what he called "Dual Momentum" in his 2014 book of the same name. This concept forms the basis of several strategies on reblnc.com, which we will explore in later articles.

How Momentum Works in Practice (With ETFs)

Modern momentum strategies do not focus on individual stocks. Instead, they rotate among broad, diversified ETFs (Exchange-Traded Funds), baskets of stocks or bonds that you can buy and sell like regular shares.

Here’s what a simple momentum process looks like:

- Step 1: At the end of each month, check how your assets performed over the past 12 months.

- Step 2: If stocks are trending up (above their 12-month average), stay invested in stocks.

- Step 3: If stocks are trending down, switch to bonds or cash for protection.

- Step 4: Among stocks that are trending up, invest in the one with the strongest momentum.

That's all there is to it. No day trading. No constantly monitoring charts. Just a calm, monthly check that takes less than 10 minutes. The discipline comes from following the signals rather than being glued to a screen.

Common Objections (And Why They Don't Hold Up)

"Isn't this just market timing?"

Sort of, but not in the way you might think. Traditional market timing tries to predict the future by guessing when the market will go up or down based on instincts or forecasts. Momentum does not try to predict; it reacts to what is already happening. It's the difference between saying, "I think it will rain tomorrow," and "It's been raining for three hours and the clouds are getting darker."

"If everyone knows about it, won't it stop working?"

This is a valid question. The momentum anomaly was first published in 1993, over 30 years ago. Yet it continues to persist. Asness and colleagues argue this is because the behavioral biases that drive momentum are deeply rooted in human nature. We will always underreact to news, follow the crowd, and sell winners too quickly. These are not flaws that education can correct; they are features of how our brains process information and emotion.

"What about the risks?"

Momentum is not risk-free. The biggest risk is a "momentum crash", a sudden reversal where yesterday's winners decline and yesterday's losers surge. This notably happened in 2009 when markets rebounded sharply from the financial crisis. However, modern strategies (like those on reblnc.com) use protective measures such as absolute momentum to minimize exposure during turbulent times. We will discuss risk management in more detail in a later article.

Key Takeaways

- Momentum is the tendency for winning assets to keep winning and losing assets to keep losing.

- It has support from over 30 years of peer-reviewed academic research across markets and countries.

- It works because of deeply rooted human behavioral biases (underreaction, herding, loss aversion).

- Unlike buy-and-hold, momentum strategies can move to safety during market downturns.

- Modern implementation uses ETFs and requires only a monthly check-in.

- It's not about predicting; it's disciplined reaction to observable market trends.

Sources & Further Reading

- Jegadeesh, N. & Titman, S. (1993). "Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency." Journal of Finance, 48(1), 65-91.

- Asness, C., Moskowitz, T. & Pedersen, L. (2013). "Value and Momentum Everywhere." Journal of Finance, 68(3), 929-985.

- Asness, C. et al. (2014). "Fact, Fiction and Momentum Investing." Journal of Portfolio Management, 40(5), 75-92.

- Antonacci, G. (2014). Dual Momentum Investing: An Innovative Strategy for Higher Returns with Lower Risk. McGraw-Hill.

- Hong, H. & Stein, J. (1999). "A Unified Theory of Underreaction, Momentum Trading and Overreaction in Asset Markets." Journal of Finance, 54(6), 2143-2184.

- Kahneman, D. & Tversky, A. (1979). "Prospect Theory: An Analysis of Decision Under Risk." Econometrica, 47(2), 263-292.

- Shiller, R. (2000). Irrational Exuberance. Princeton University Press.

- Geczy, C. & Samonov, M. (2016). "Two Centuries of Price-Return Momentum." Financial Analysts Journal, 72(5), 32-56.

- Rouwenhorst, K.G. (1998). "International Momentum Strategies." Journal of Finance, 53(1), 267-284.

Subscribe to our research

Get the latest tactical allocation strategies and academic whitepapers delivered to your inbox.