Here's a puzzle that should bother efficient market believers: momentum has been documented in academic literature since 1993, replicated across dozens of asset classes and time periods, published in the most prestigious finance journals — and it still works. If markets were truly efficient, the moment this anomaly became known, arbitrageurs would trade it away. They haven't. The reason tells you something fundamental about what actually drives markets: human psychology.

Why Anomalies Persist: The Limits of Arbitrage

Before diving into the specific biases, it's worth understanding why knowing about a market anomaly doesn't automatically eliminate it. Academic economists Eugene Fama and Kenneth French built the efficient market hypothesis on the idea that arbitrageurs would quickly close any pricing gaps. But real-world arbitrage has limits:

- Timing risk: You can be right about a trend but wrong about when it reverses. Momentum traders can suffer years of underperformance before the anomaly reasserts itself.

- Career risk: Fund managers who pursue 'irrational' strategies can lose clients before the strategy pays off, even if the long-term logic is sound.

- Capacity constraints: As more capital piles into momentum, the signal weakens. But the supply of new behavioral biases is effectively unlimited — humans keep making the same mistakes generation after generation.

Shiller (2000) in 'Irrational Exuberance' demonstrated that psychological factors drive sustained mispricings that rational arbitrage fails to correct. Momentum is perhaps the clearest example.

The Four Biases That Create Momentum

Bias 1: Anchoring and Insufficient Adjustment

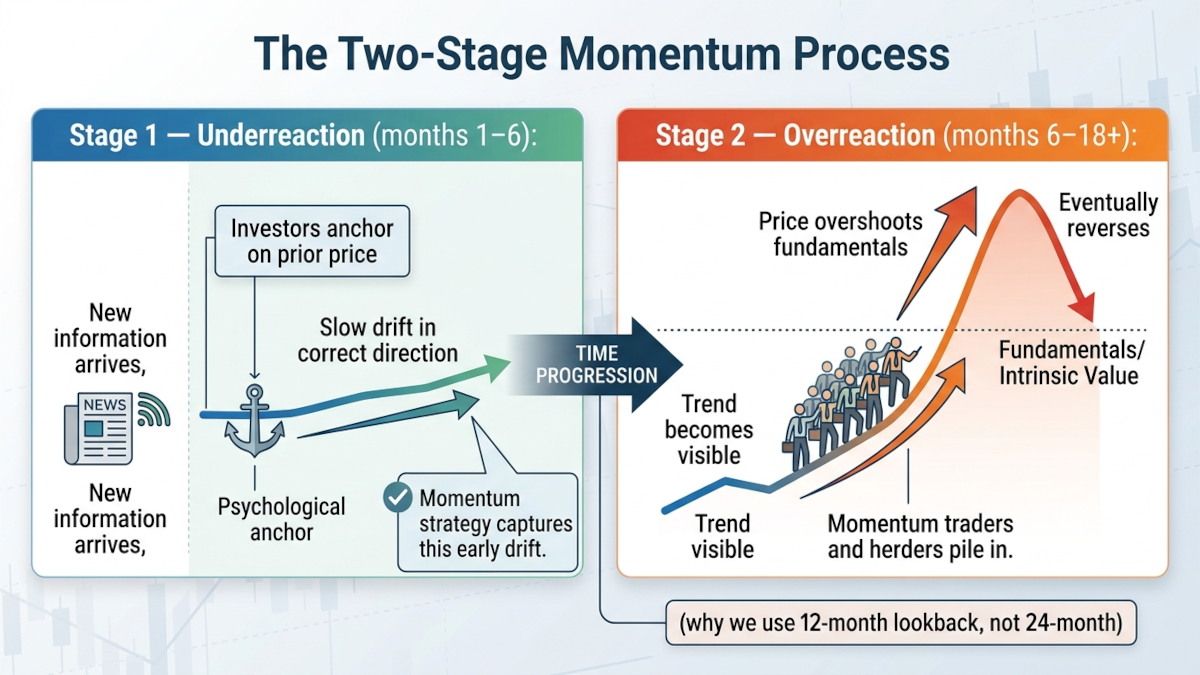

When investors receive new information — an earnings beat, a central bank decision, a technological breakthrough — they don't immediately reprice the asset to reflect that information fully. Instead, they anchor on the prior price and adjust insufficiently.

Kahneman and Tversky's foundational 1979 paper 'Prospect Theory: An Analysis of Decision Under Risk' demonstrated this experimentally: people systematically underweight new information relative to prior beliefs. In markets, this creates underreaction — prices move in the right direction but not far enough, leaving a predictable drift that momentum strategies capture.

Think of a company that reports earnings 20% above consensus. The rational response is an immediate 20% price jump. What actually happens: a 10% jump on earnings day, then a slow drift upward over the following months as analysts revise forecasts and more investors update their views. Momentum investors ride that drift.

Bias 2: The Herding Effect and Overreaction

If underreaction creates early momentum, herding amplifies and extends it. Once a trend is established, investors pile in — not because the fundamentals support the price, but because other investors are buying, creating social proof.

Hong and Stein (1999) in 'A Unified Theory of Underreaction, Momentum Trading, and Overreaction in Asset Markets' modeled this two-stage process formally: information diffuses slowly through the market (creating underreaction and early momentum), then momentum traders pile in (creating overreaction and eventual reversal). Their model explains why momentum strategies have historically worked best over the 3–12 month window: long enough to capture the information diffusion phase, short enough to avoid the reversal phase.

The herding bias is deeply cultural. During bull markets, not owning the hot asset feels like leaving money on the table. During bear markets, everyone selling creates panic disproportionate to fundamentals. Both directions create momentum.

Source: Source: Hong & Stein (1999)

Source: Source: Hong & Stein (1999)

Bias 3: The Disposition Effect

The disposition effect, named by Shefrin and Statman (1985) and deeply grounded in Kahneman & Tversky's prospect theory, describes investors' tendency to sell winners too early and hold losers too long.

Prospect theory explains why: losses feel roughly twice as painful as equivalent gains feel good. So investors lock in gains quickly (to 'bank' the good feeling) and hold losses (to avoid the pain of realizing them). The result: winning assets are persistently undersupplied as holders sell too soon, creating upward price pressure. Losing assets are persistently oversupplied as holders refuse to sell, creating downward price pressure. Both effects are momentum.

Daniel, Hirshleifer, and Subrahmanyam (1998) in 'Investor Psychology and Security Market Under- and Overreactions' showed how self-attribution bias compounds this: investors take credit for winning trades (confirming their view), which increases overconfidence and further extends momentum.

Bias 4: The Confirmation Bias Loop

Once a trend is in place, it creates a self-reinforcing cycle. Rising prices attract media coverage. Media coverage attracts new investors. New investors validate the trend for existing investors. Existing investors add to positions. This feedback loop is most visible in speculative bubbles, but it operates at a smaller scale in virtually every trending market.

Robert Shiller's Nobel Prize-winning research documented what he called 'narrative economics' — the role of popular stories in driving asset prices. A compelling narrative (AI will transform everything; this commodity will run out; this country is the next growth engine) attracts capital independently of whether the fundamentals support current prices. Momentum strategies ride these narratives during their ascent and exit before the reversal.

Why These Biases Don't Get Arbitraged Away

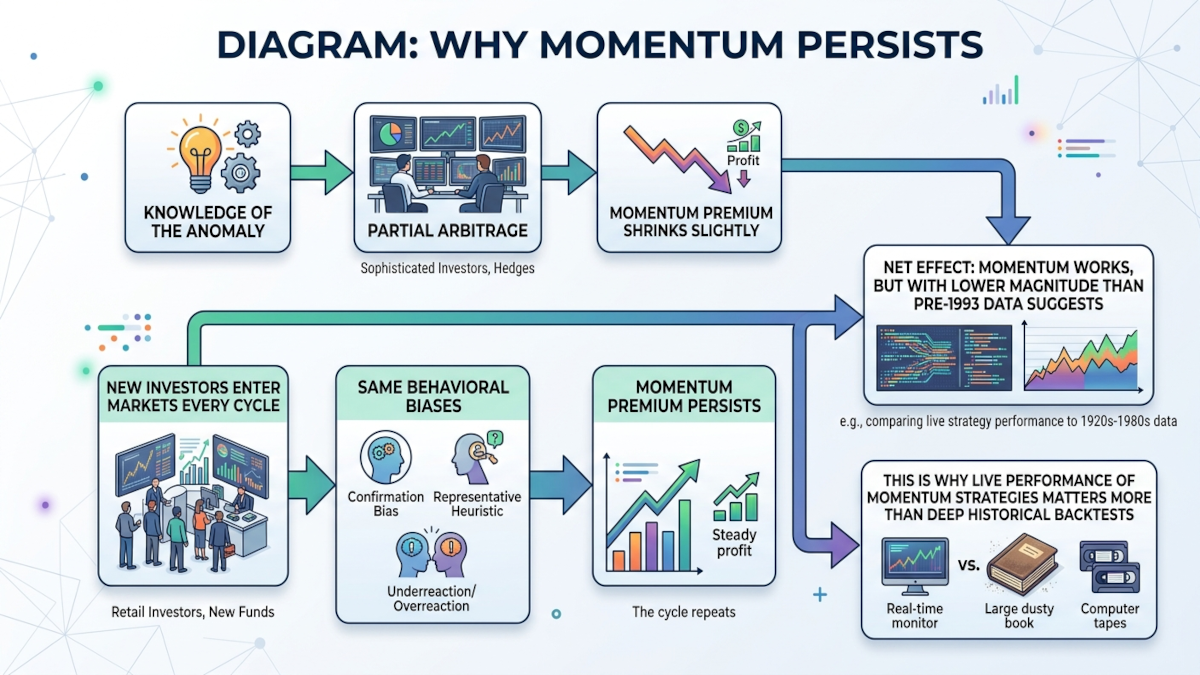

The critical question: if sophisticated institutional investors know about these biases, why don't they trade against them and eliminate the anomaly?

Three reasons:

First, timing is brutal. You can know a stock is overvalued due to herding but still lose money for 18 months while the herding continues. As Keynes observed (and as documented rigorously by Shleifer and Vishny in their 1997 paper on the limits of arbitrage): 'Markets can remain irrational longer than you can remain solvent.'

Second, momentum is self-defeating at scale. If a fund grows large enough, buying momentum stocks moves prices against itself. This capacity constraint means that beyond a certain fund size, momentum strategies become less effective. Large funds rationally avoid strategies that their own size would destroy.

Third, the biases are structural. These aren't errors that education eliminates. Kahneman (who won the Nobel Prize in Economics in 2002) spent decades trying to help people make better decisions and documented that knowing about cognitive biases reduces but doesn't eliminate them. The disposition effect persists among professional traders who have been told about it and understand it academically. Momentum's fuel source is self-replenishing.

Behavioral Finance Meets the Momentum Lookback

Understanding the behavioral drivers helps explain GEM's specific design choices:

Why 12 months and not 6 or 24? The 1–12 month window captures the underreaction/information diffusion phase before the overreaction/herding phase typically peaks. Academic research by Jegadeesh and Titman (1993, 2001) showed that momentum signals are strongest at 3–12 months and reverse at 24–36 months (the 'long-run reversal' documented by De Bondt and Thaler). The behavioral story maps directly onto this: information diffuses for months (creating the profitable drift), then overshoots (eventually reversing).

Why does absolute momentum work? Because investor sentiment at the market level also follows behavioral patterns — bull market overconfidence creates extended uptrends; bear market panic creates extended downtrends. Absolute momentum (comparing returns to T-bills) captures whether the overall sentiment is positive or negative, not just which asset is most popular.

The Persistence Paradox

There's a genuine puzzle here: if momentum is so well-documented and so clearly behavioral in origin, why hasn't it been traded away in the 30+ years since Jegadeesh and Titman published it?

AQR's research team has argued that momentum returns have declined modestly since publication but remain positive and significant. Their 2017 analysis found momentum premia across asset classes were still present, though smaller than in pre-publication data — consistent with partial arbitrage but not elimination.

The most compelling explanation: behavioral biases are structural features of human cognition, not correctable errors. Every generation of investors makes the same mistakes. Every market cycle, the same anchoring and herding patterns emerge. As long as humans are making investment decisions — and even as algorithms trained on human data are making them — the fuel for momentum will persist.

Practical Implications for Your Strategy

This behavioral analysis has direct implications for how you use reblnc:

Expect underperformance during low-behavioral-divergence markets. When markets are rational — no extreme narratives, balanced investor sentiment — behavioral momentum is weak. The 2014–2021 US bull market had periods of remarkably steady rational accumulation without the panics and manias that create the strongest momentum signals.

Don't try to predict when momentum will work. The behavioral biases that create momentum are not predictable in their timing. A rules-based monthly rebalancing approach (like GEM, HAA, or DAA on reblnc) is more robust than trying to time when human psychology will be most irrational.

Your biggest risk is your own psychology. The hardest part of momentum investing isn't the signal — it's following it. When GEM or HAA says 'move to bonds' during a bull market, the psychological pressure to stay in equities is enormous. You're fighting the same herding instinct that creates the momentum you're trying to exploit.

Key Takeaways

- Momentum persists because human cognitive biases — anchoring, herding, disposition effect — are structural, not correctable errors

- Underreaction (anchoring on old prices) creates early momentum; overreaction (herding) extends and amplifies it

- The 12-month lookback captures the information-diffusion phase before the overreaction reversal — grounded in behavioral theory, not data-fitting

- Sophisticated investors can't easily arbitrage momentum away due to timing risk, career risk, and capacity constraints

- Prospect theory explains the disposition effect: investors sell winners too soon and hold losers too long, creating persistent mispricings

- Momentum premia have declined modestly since publication but persist because behavioral biases are self-replenishing — each new generation makes the same mistakes

- Your biggest edge isn't the signal — it's the discipline to follow it when it's most uncomfortable

Sources & Further Reading

- Kahneman, D., & Tversky, A. (1979). 'Prospect Theory: An Analysis of Decision Under Risk.' Econometrica, 47(2), 263–291.

- Jegadeesh, N., & Titman, S. (1993). 'Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency.' Journal of Finance, 48(1), 65–91.

- Hong, H., & Stein, J.C. (1999). 'A Unified Theory of Underreaction, Momentum Trading, and Overreaction in Asset Markets.' Journal of Finance, 54(6), 2143–2184.

- Daniel, K., Hirshleifer, D., & Subrahmanyam, A. (1998). 'Investor Psychology and Security Market Under- and Overreactions.' Journal of Finance, 53(6), 1839–1885.

- Shiller, R.J. (2000). Irrational Exuberance. Princeton University Press.

- Shefrin, H., & Statman, M. (1985). 'The Disposition to Sell Winners Too Early and Ride Losers Too Long.' Journal of Finance, 40(3), 777–790.

- Asness, C., Frazzini, A., Israel, R., & Moskowitz, T. (2015). 'Fact, Fiction, and Momentum Investing.' Journal of Portfolio Management, 40(5), 75–92.

Subscribe to our research

Get the latest tactical allocation strategies and academic whitepapers delivered to your inbox.