Antonacci's GEM was the strategy that made dual momentum mainstream. The versions running on reblnc.com today, HAA and DAA-G12, came after. Understanding why requires understanding where GEM ran into trouble.

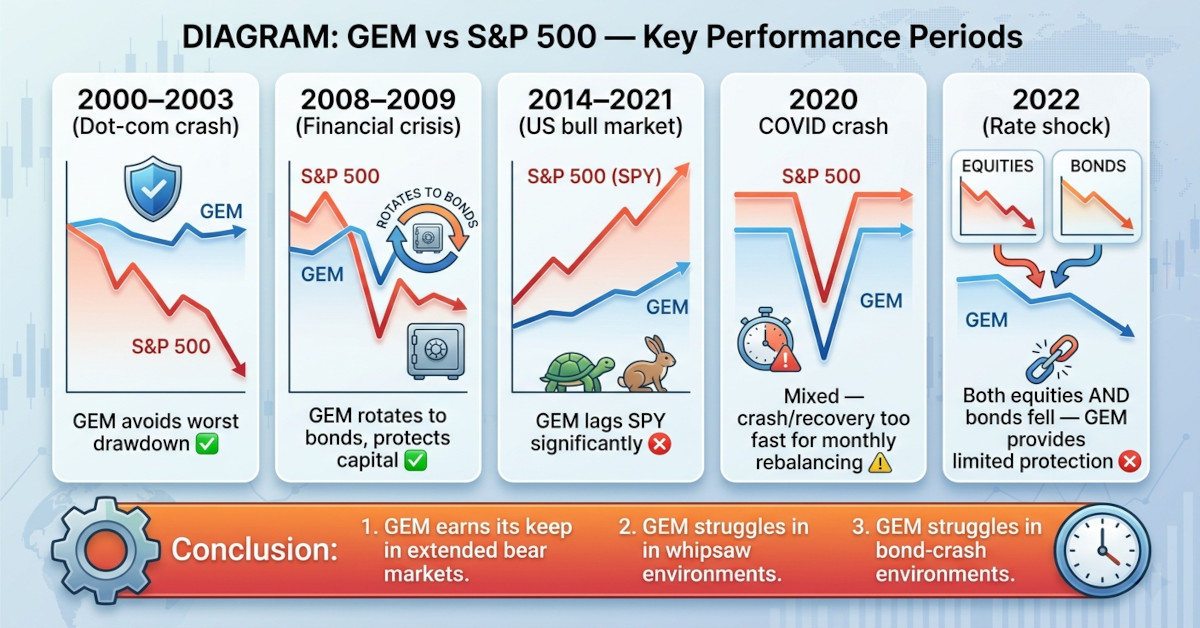

GEM's decade of struggle: 2014–2022

If you had implemented GEM in early 2014, following Antonacci's book release, you would have underperformed a simple SPY (the S&P 500 ETF — it tracks the 500 largest US companies) buy-and-hold for most of the next eight years. This is uncomfortable but worth understanding.

Three structural problems drove the underperformance:

Problem 1: The US dominance problem

GEM compares US equities (SPY) against international equities (EFA — the MSCI EAFE index, covering developed markets in Europe, Asia, and Australia). From 2014 to 2021, US equities dominated international in a way that was historically unusual. Apple, Microsoft, Amazon, and Google drove returns that no international index could match. GEM correctly allocated to SPY over EFA most of this period, but SPY itself underperformed in some GEM-rotation windows when the timing was off.

More critically, when the absolute momentum signal fired and GEM moved to bonds (AGG — the iShares Core US Aggregate Bond ETF, a broad US bond market fund), the US market often recovered quickly. You'd exit into bonds and re-enter equities at a higher price. These are whipsaw trades, and they add up.

Problem 2: Excessive defensiveness

GEM's absolute momentum rule, comparing the equity winner against T-bills, is a single binary signal. Either you're fully in equities or you're fully in bonds. When markets were choppy but not decisively bearish (2015–2016, late 2018), GEM oscillated in and out of bonds, incurring transaction friction and missing rallies.

Keller & Keuning's 2022 paper "Breadth Momentum and the Canary Universe" quantified this: strategies that use multiple defensive signals rather than a single binary switch had better risk-adjusted returns across the same historical period.

Problem 3: The 2022 bond problem

In 2022, when the Federal Reserve raised rates aggressively, both equities and bonds fell simultaneously. GEM's defensive asset, AGG, lost about 13% that year. A strategy designed to protect capital by moving to bonds provided essentially no protection.

This wasn't a flaw Antonacci could have anticipated from pre-2000 data. Bonds and equities rarely fell together before 2022. But it exposed a real limitation.

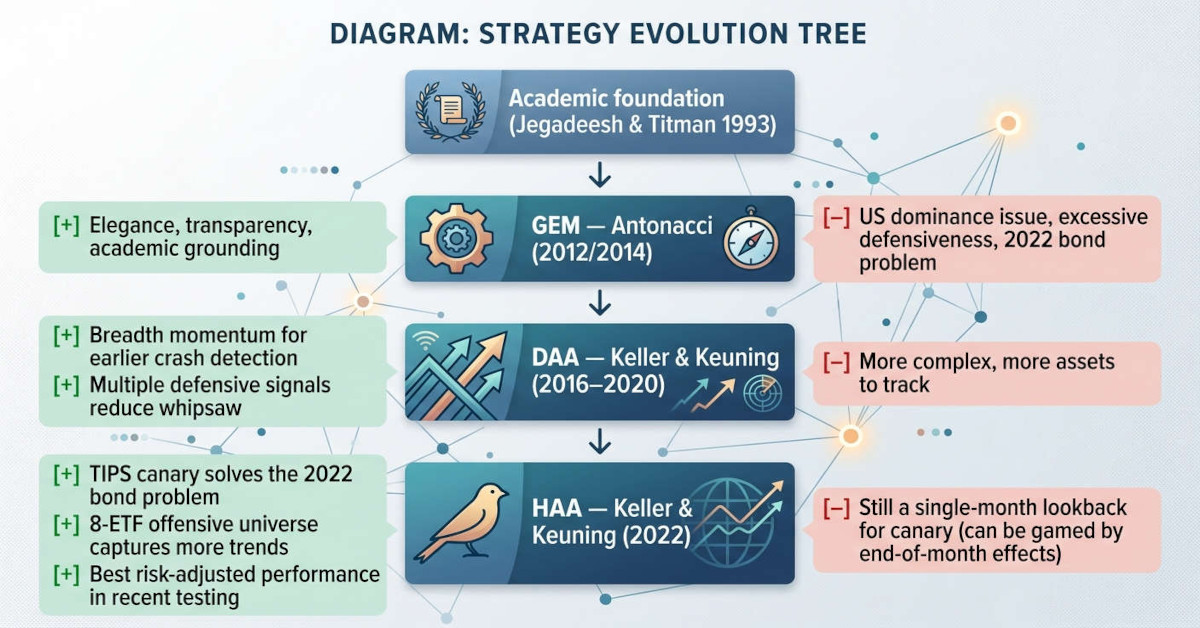

Enter Wouter Keller

Dutch researcher Wouter Keller, working with Jan Willem Keuning, published a series of papers that directly addressed these problems. Their work, particularly the Defensive Asset Allocation (DAA) series and the 2022 Hybrid Asset Allocation (HAA) paper, moved momentum strategy design forward in ways GEM hadn't.

The core idea: instead of using a single asset's absolute momentum as the defensive signal, use a small set of risk indicators whose collective behavior provides earlier warning of market stress. Keller called this the "canary universe."

Defensive Asset Allocation (DAA): breadth as early warning

DAA uses breadth momentum across a universe of risky assets as its crash-detection mechanism. Instead of asking "is SPY above its 12-month average?", it asks: how many assets in a broad global universe have positive momentum?

When market stress builds, it tends to show up across many asset classes at once. Emerging markets, high-yield bonds, commodities, and developed market equities often start declining together. By monitoring breadth across a 12-asset universe (hence DAA-G12), the strategy can detect systemic risk earlier than any single-asset signal.

In practice, DAA historically rotates to defensive assets (bills, bonds, gold) before the worst of major drawdowns, with fewer false alarms than GEM's binary switch.

Hybrid Asset Allocation (HAA): the TIPS canary

HAA, published in 2022, addressed a different problem: what defensive asset actually holds up when both stocks and bonds fall?

Keller's answer was to use Treasury Inflation-Protected Securities (TIPS) not as a defensive asset, but as an early warning signal. HAA uses a single TIPS ETF (ticker: TIP — iShares TIPS Bond ETF) as its canary. When TIP has negative momentum, meaning real yields are rising and creating the environment where both stocks and bonds struggle, HAA moves entirely to cash or short-term bills.

In 2022, HAA's TIPS canary would have flagged danger early in the year, moving the strategy to cash before the worst of the drawdown. That's the difference from GEM: GEM asks "are equities trending?" and HAA asks "is the environment one where owning assets at all makes sense?"

The full HAA strategy uses an 8-ETF offensive universe covering global equities, bonds, gold, and real estate, ranking them by momentum and selecting the top one or two. The TIPS canary determines whether to run offense or defense. The dedicated HAA Deep Dive covers the full mechanics.

From two assets to universes

GEM's appeal was its simplicity: three ETFs, one decision rule. HAA and DAA use more assets and more signals, but they're still rules-based and systematic.

The added complexity isn't arbitrary. Each additional element addresses a specific failure mode of simpler strategies:

- Multiple defensive indicators instead of a single signal reduce false defensive moves

- A broader offensive universe captures more trend opportunities than a US/international binary

- A TIPS-based canary provides better crash detection in rate-shock environments than comparing against T-bills

- More gradual allocation shifts make transitions smoother

Whether that trade-off is worth it depends on you. More moving parts also means more opportunities for execution error.

The strategy landscape today

What the research actually shows

Keller & Keuning's 2022 paper ran extensive backtests comparing these approaches across multiple market regimes. DAA consistently reduced maximum drawdown relative to GEM. HAA showed better Sharpe ratios in the 2014–2022 period, mostly due to the improved defensive mechanism. The breadth momentum approach (multiple signals rather than one) held up as a real improvement rather than a backtest artifact.

Keller also published his papers on SSRN before the strategies gained wide attention, which matters for evaluating whether the results are genuine. Allocate Smartly has tracked these strategies independently, monitoring out-of-sample performance alongside dozens of other tactical approaches.

The honest caveats

HAA and DAA have shorter live track records than GEM. GEM has been tracked out-of-sample since 2012. HAA's 2022 paper means it has roughly two or three years of true out-of-sample performance. The backtests are compelling, but backtests can be shaped even when researchers are trying hard to avoid it.

Complexity has costs too. More ETFs means more rebalancing decisions, more potential for execution errors, and more surface area for strategy drift. GEM's three-ETF simplicity is a real advantage if you want minimal maintenance and fewer judgment calls.

And no strategy handles regime change gracefully. HAA's TIPS canary would have helped in 2022. But if the next crisis arrives through crypto contagion, a geopolitical shock, or something else that doesn't resemble past market stress, historical performance says little about what to expect.

Which strategy is right for you?

This article is a roadmap, not a recommendation. The right strategy depends on your risk tolerance, tax situation, time commitment, and, honestly, how confident you are in your ability to stick with a strategy during the periods when it's underperforming.

The dedicated deep dives cover the mechanics in detail. HAA Deep Dive covers the TIPS canary and the 8-ETF universe. DAA-G12 Deep Dive covers breadth momentum and the 12-asset global universe. reblnc.com lets you run comparative backtests across all strategies with identical time periods and metrics.

Key takeaways

- GEM underperformed from 2014–2021 because of US equity dominance and whipsaw trades during a historically long bull run, not because the strategy is broken

- 2022 exposed GEM's main weak point: bonds fell alongside equities, making the defensive asset ineffective

- DAA addressed this by using breadth momentum across many assets rather than a single signal

- HAA's TIPS canary was specifically designed to detect rate-shock environments where stocks and bonds fall together

- The progression from GEM to DAA to HAA is iterative improvement, not reinvention; the core momentum logic carries through

- HAA and DAA have shorter live records, and compelling backtests still need out-of-sample validation

- Use reblnc.com's comparative backtest to evaluate all strategies on equal terms before committing

Sources & Further Reading

- Antonacci, G. (2014). Dual Momentum Investing. McGraw-Hill Education.

- Keller, W., & Keuning, J.W. (2016). "Protective Asset Allocation (PAA): A Simple Momentum-Based Alternative for Term Deposits." SSRN Working Paper #2759734.

- Keller, W., & Keuning, J.W. (2018). "Breadth Momentum and Vigilant Asset Allocation." SSRN Working Paper #3002624.

- Keller, W., & Keuning, J.W. (2022). "Breadth Momentum and the Canary Universe: Defensive Asset Allocation." SSRN Working Paper #3383232.

- Allocate Smartly. (2024). "Hybrid Asset Allocation — Strategy Overview." allocatesmartly.com

- Allocate Smartly. (2024). "Global Equity Momentum — Strategy Overview." allocatesmartly.com

Subscribe to our research

Get the latest tactical allocation strategies and academic whitepapers delivered to your inbox.