Imagine finding a trading rule that an independent researcher backtested across 40 years of data, published openly, and then watched beat the market for several years running. That's the story of Gary Antonacci's Global Equity Momentum. The rules are almost absurdly simple: two ETF comparisons, monthly. The strategy is specific enough to be auditable and grounded enough in academic research that it has become the default benchmark for tactical ETF approaches built since.

Who Is Gary Antonacci?

Gary Antonacci is not a Wall Street insider. He spent decades working through the academic literature on market anomalies before publishing his framework as a 2012 SSRN paper, "Risk Premia Harvesting Through Dual Momentum", later expanded into his 2014 book Dual Momentum Investing. The paper introduced a disciplined, rules-based system combining two previously separate momentum concepts into one coherent approach.

Antonacci didn't discover momentum. Academics had been documenting it since at least 1993. His contribution was combining relative momentum (which asset is strongest?) with absolute momentum (is the strongest asset worth owning at all?) into what he called Dual Momentum. That combination is what makes GEM more than just a rotation strategy.

The Academic Foundation

Momentum as a market anomaly was established by Jegadeesh and Titman in their 1993 study, confirmed again in their 2001 paper "Profitability of Momentum Strategies: An Evaluation of Alternative Explanations." They showed that stocks performing well over the past 3-12 months continued to outperform over the following 3-12 months, a finding that held across decades of data and was awkward for efficient market theorists to explain.

AQR Capital's 2014 paper "The Case for Momentum" (Asness, Moskowitz, and Pedersen) extended this across global stocks, bonds, commodities, and currencies. Momentum wasn't a US quirk.

"Momentum is the premier market anomaly. It is the strongest effect in the data, cutting across asset classes, and has no serious risk-based explanation." — Cliff Asness, AQR Capital, 2014

Antonacci built directly on this research. His contribution was making it executable for retail investors: monthly rebalancing, two or three ETFs, no complex calculations.

The Two Pillars of Dual Momentum

Relative Momentum (Cross-Sectional)

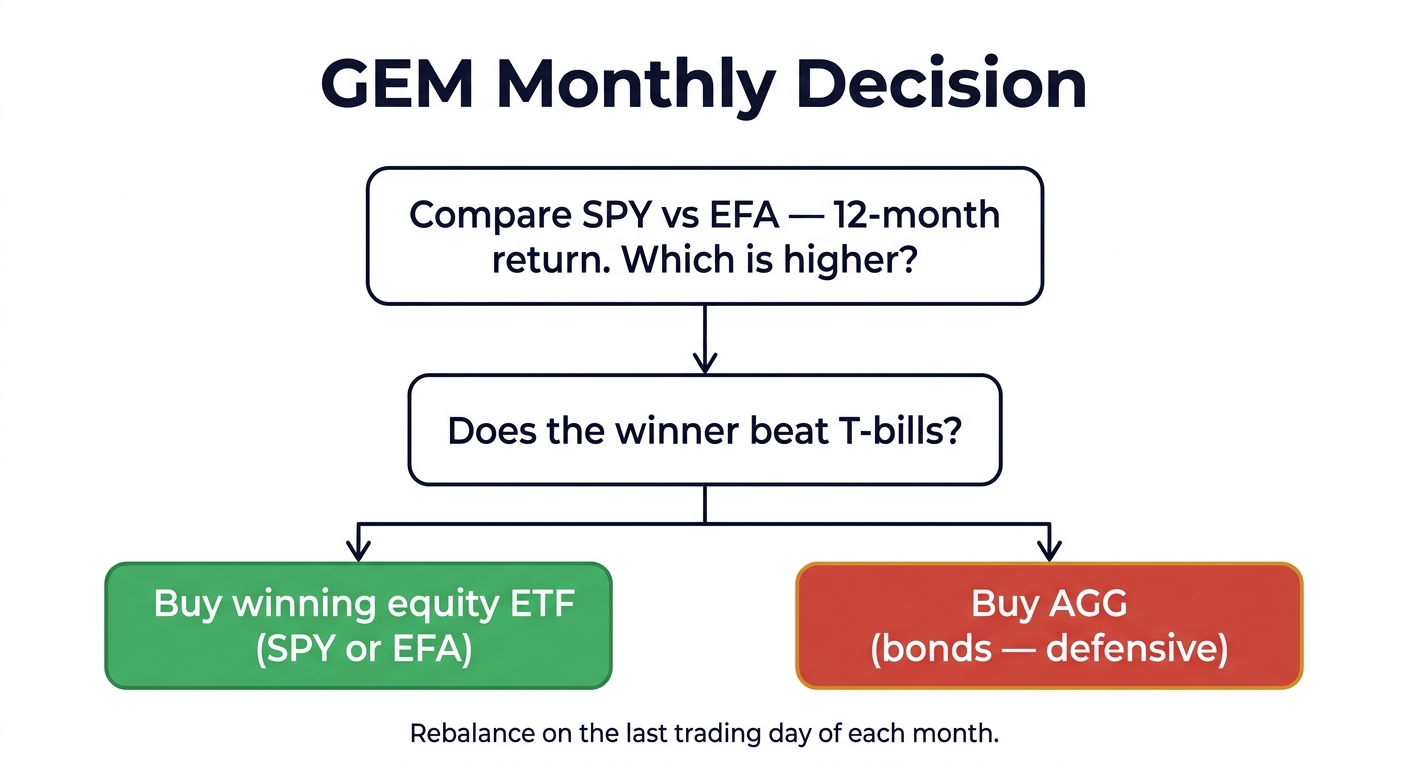

Relative momentum is a comparison: among a set of assets, which one has performed best? In GEM, it's US equities (SPY) vs. international equities (EFA). Whichever has the higher 12-month return gets the allocation. That's it.

This is the "dual" in Dual Momentum. Instead of just buying whatever has gone up, you compare assets against each other and pick the stronger one.

Absolute Momentum (Time-Series)

Absolute momentum asks a different question: is the winner actually worth owning, or should we sit this one out? The test is simple: compare the winning asset's 12-month return against T-bills. If US equities beat international equities AND beat T-bills, buy US equities. If both equity ETFs lose to T-bills, move to defensive bonds (AGG).

This is the crash-protection mechanism. When both stock markets are falling hard, the rule is: neither. Go to bonds.

The Original Backtest Results

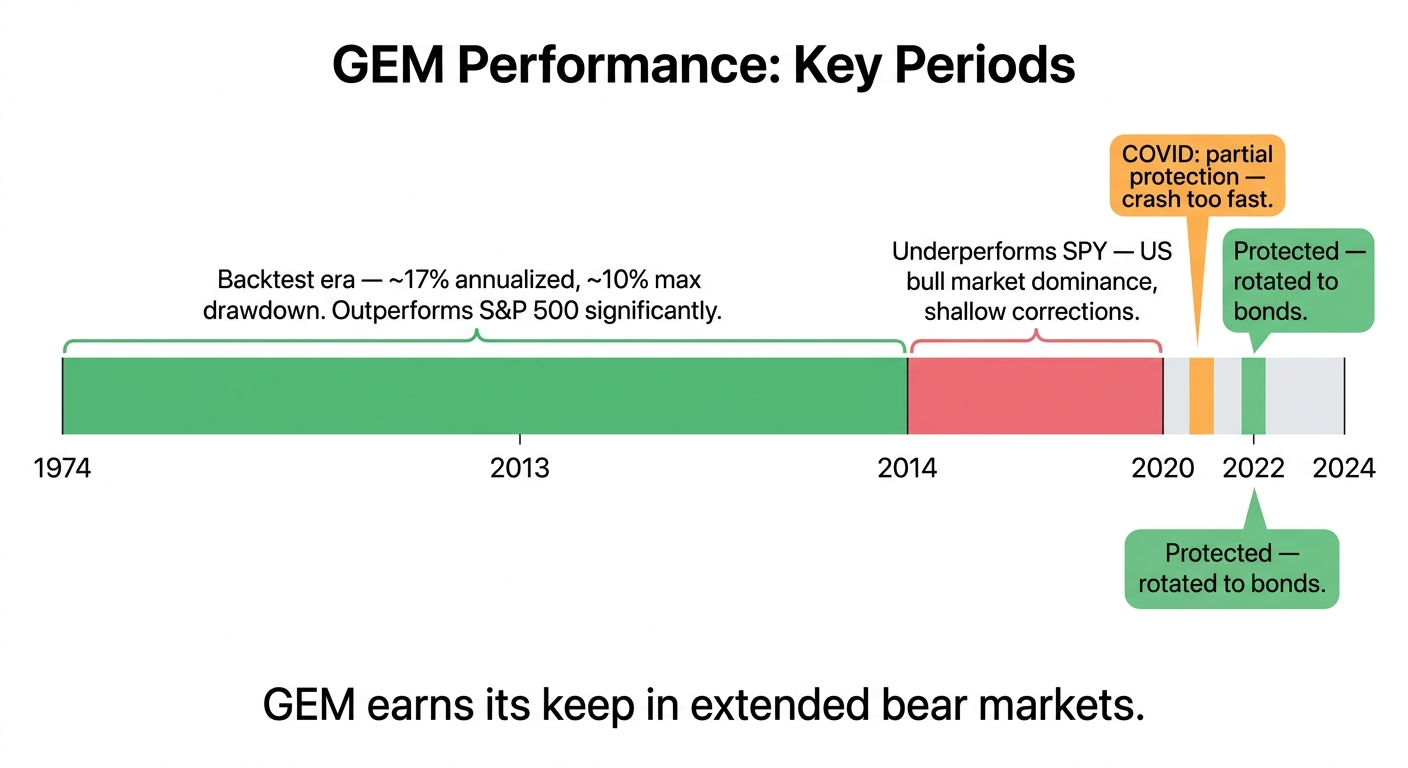

Antonacci's backtest covered 1974-2013, nearly four decades. The numbers:

- GEM: ~17% annualized return, ~10% max drawdown

- S&P 500 buy-and-hold: ~10% annualized return, ~51% max drawdown

- 60/40 portfolio: ~10% annualized return, ~27% max drawdown

The return difference is good, but the drawdown comparison is what matters. GEM's worst peak-to-trough loss was roughly 10%, versus 51% for buy-and-hold during the 2000-2002 and 2008-2009 crashes. That's what the absolute momentum component buys you: the strategy rotates to bonds before the worst losses materialize.

Antonacci didn't pick a favorable period. The backtest ran through the 1970s inflation crisis, the dot-com crash, the 2008 financial crisis, and extended bull markets in between. The defensive mechanism worked in each major bear market by rotating out of equities before the full drawdown hit.

Post-Publication Performance: The Reality Check

Here's where honesty matters more than cheerleading. GEM was published in 2012, with the book following in 2014. What happened over the next decade was not great for the strategy.

From 2014 to 2022, GEM underperformed a simple S&P 500 buy-and-hold. The reasons are straightforward:

- The US bull market ran for years with shallow corrections, so GEM's defensive mechanism rarely triggered

- When GEM did rotate to international equities, EFA significantly underperformed SPY (the US dominance during that period was unusual by historical standards)

- Whipsaw trades, brief signals that reversed quickly, generated transaction costs and caused the strategy to miss parts of rallies

This is expected behavior for any trend-following approach. Long bull markets with shallow drawdowns are the worst-case scenario for absolute momentum strategies. The strategy protects against extended crashes; it wasn't designed to maximize returns when the S&P 500 goes up almost every year.

GEM did what it was supposed to in 2020: it rotated to bonds in March 2020 ahead of the sharpest part of the crash, then rotated back to equities in April as the recovery began. The problem was that the crash and recovery were both so fast that some investors missed the rotation entirely. That's an honest limitation.

Why GEM Remains the Reference Strategy

Despite the rough post-publication decade, GEM is still the benchmark that tactical strategies get compared against.

The rules are fully explicit. 12-month lookback, monthly rebalancing, three ETFs. You can replicate it on a spreadsheet in an afternoon. That level of transparency is rare in systematic investing, since most strategies involve enough discretion that you can't fully audit what you're running.

The theoretical basis is solid. GEM isn't a curve-fitted pattern discovered by mining historical data. It's built on academic anomalies (relative and absolute momentum) that have been replicated independently across asset classes, time periods, and research teams. The anomaly was documented first and the strategy was built on top of it.

GEM's specific weaknesses also directly shaped what came next. Wouter Keller's HAA and DAA strategies were designed to address exactly the failure modes GEM exposed: excessive defensiveness, poor US/international signal timing, and whipsaw risk. You can't make sense of HAA without understanding GEM first.

The Parameters That Matter

The 12-Month Lookback

The 12-month lookback wasn't chosen to fit the backtest. Academic research consistently shows that the 1-12 month window is where momentum is strongest. The 1-month return is often reversed by short-term mean reversion, and lookbacks beyond 12 months start capturing mean-reversion rather than momentum. 12 months was already identified in the literature as the sweet spot before Antonacci built his strategy around it.

Monthly Rebalancing

Monthly rebalancing is a trade-off between responsiveness and transaction costs. Weekly rebalancing creates more whipsaw trades; quarterly is too slow to catch major trend shifts. Monthly has become the standard for tactical ETF strategies, largely because of GEM.

The Defensive Asset

GEM uses AGG (aggregate bond index) as its defensive holding. Bonds historically have low correlation with equities, which makes them useful protection during equity bear markets. But 2022 exposed the flaw: when both stocks and bonds fall together because of rising interest rates, AGG doesn't help. This is part of why newer strategies have moved toward TIPS or cash as alternatives.

How to Implement GEM on reblnc.com

reblnc.com handles the monthly calculation automatically. Each month, the platform calculates 12-month returns for SPY, EFA, and T-bills, applies Antonacci's rules, and shows you the current signal. The backtest page displays Sharpe ratio, max drawdown, and CAGR across multiple time periods.

What reblnc doesn't do: it doesn't execute trades. The signal tells you what to hold, you place the order in your own brokerage. Most users spend about five minutes a month on this.

Key Takeaways

- Dual Momentum combines relative momentum (which asset is strongest?) with absolute momentum (is it worth owning at all?)

- GEM uses three ETFs: SPY, EFA, AGG, with T-bills as the absolute momentum benchmark

- The 1974-2013 backtest showed ~17% annualized returns vs ~10% for buy-and-hold, with much lower drawdowns

- From 2014 to 2021, GEM underperformed during the US-dominated bull market — this is how the strategy is supposed to behave, not a sign it's broken

- GEM is the reference strategy because its rules are fully auditable and its theoretical basis is documented independently of the backtest

- Its specific weaknesses — excessive defensiveness, bond correlation in rising rate environments — directly shaped HAA and DAA

- The 12-month lookback and monthly rebalancing come from academic evidence, not parameter fitting

Sources & Further Reading

- Antonacci, G. (2012). "Risk Premia Harvesting Through Dual Momentum." SSRN Working Paper #2042750.

- Antonacci, G. (2014). Dual Momentum Investing: An Innovative Strategy for Higher Returns with Lower Risk. McGraw-Hill Education.

- Jegadeesh, N., & Titman, S. (2001). "Profitability of Momentum Strategies: An Evaluation of Alternative Explanations." Journal of Finance, 56(2), 699-720.

- Asness, C., Moskowitz, T., & Pedersen, L. (2013). "Value and Momentum Everywhere." Journal of Finance, 68(3), 929-985.

- AQR Capital Management. (2014). "The Case for Momentum." AQR White Paper.

- Antonacci, G. optimalmomentum.com — ongoing performance tracking and commentary

Subscribe to our research

Get the latest tactical allocation strategies and academic whitepapers delivered to your inbox.