Quick Recap: What Is Momentum?

In previous articles, we covered the basic idea: winners tend to keep winning. Assets that performed well over the past several months tend to continue outperforming, and laggards tend to keep lagging. This pattern shows up across decades of data and in markets around the world (Asness et al., 2013).

But there are actually two types of momentum, and they answer different questions. The difference matters because one picks winners while the other keeps you out of trouble.

Absolute Momentum: “Should I Be in the Market at All?”

Imagine you’re at the beach, deciding whether to go for a swim. Before you dive in, you check one thing: is the tide rising or falling? If the water is receding and conditions look rough, you stay on the shore — regardless of how good a swimmer you are.

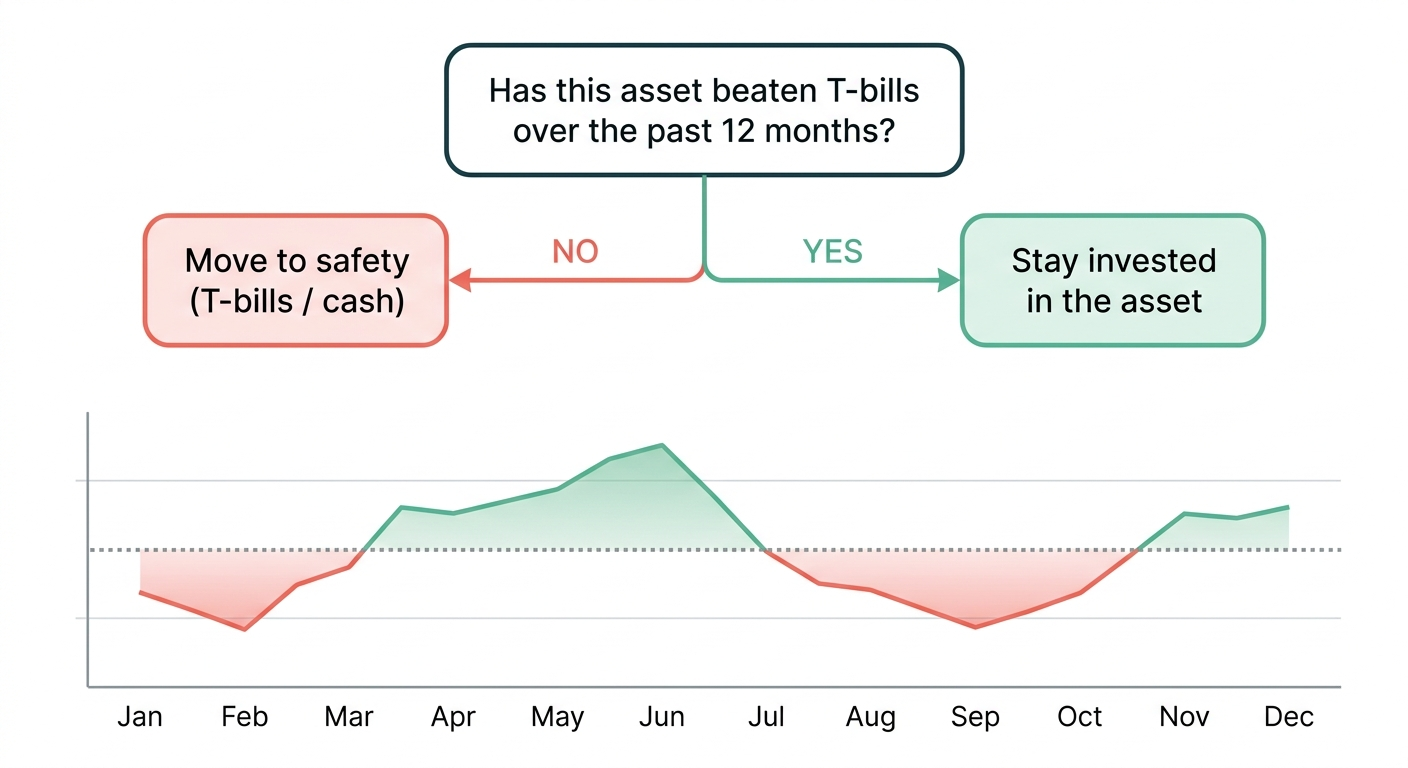

Absolute momentum asks a yes-or-no question: has this asset gone up or down over a recent lookback period (typically 12 months)? You compare the asset's return to a safe alternative, like short-term Treasury bills. If the asset beat the safe option, you stay invested. If it didn't, you move to safety.

Absolute momentum asks a simple yes-or-no question: has this asset gone up or down over a recent lookback period (typically 12 months)? More specifically, you compare the asset’s return to a safe alternative — like short-term Treasury bills (essentially cash). If the asset beat the safe option, you stay invested. If it didn’t, you move to safety.

Researchers call this "time series momentum" because you're looking at how a single asset moves through time, comparing it only against itself and a risk-free benchmark. Moskowitz, Ooi, and Pedersen (2012) showed that this signal works across 58 different markets, including equities, currencies, commodities, and bonds. Assets trending upward tended to keep going up, and assets trending downward tended to keep falling.

What makes absolute momentum useful is its defensive side. When markets are falling, this signal gets you out. Not by predicting the crash, but by reacting to the trend already underway.

Relative Momentum: “Where Should I Invest?”

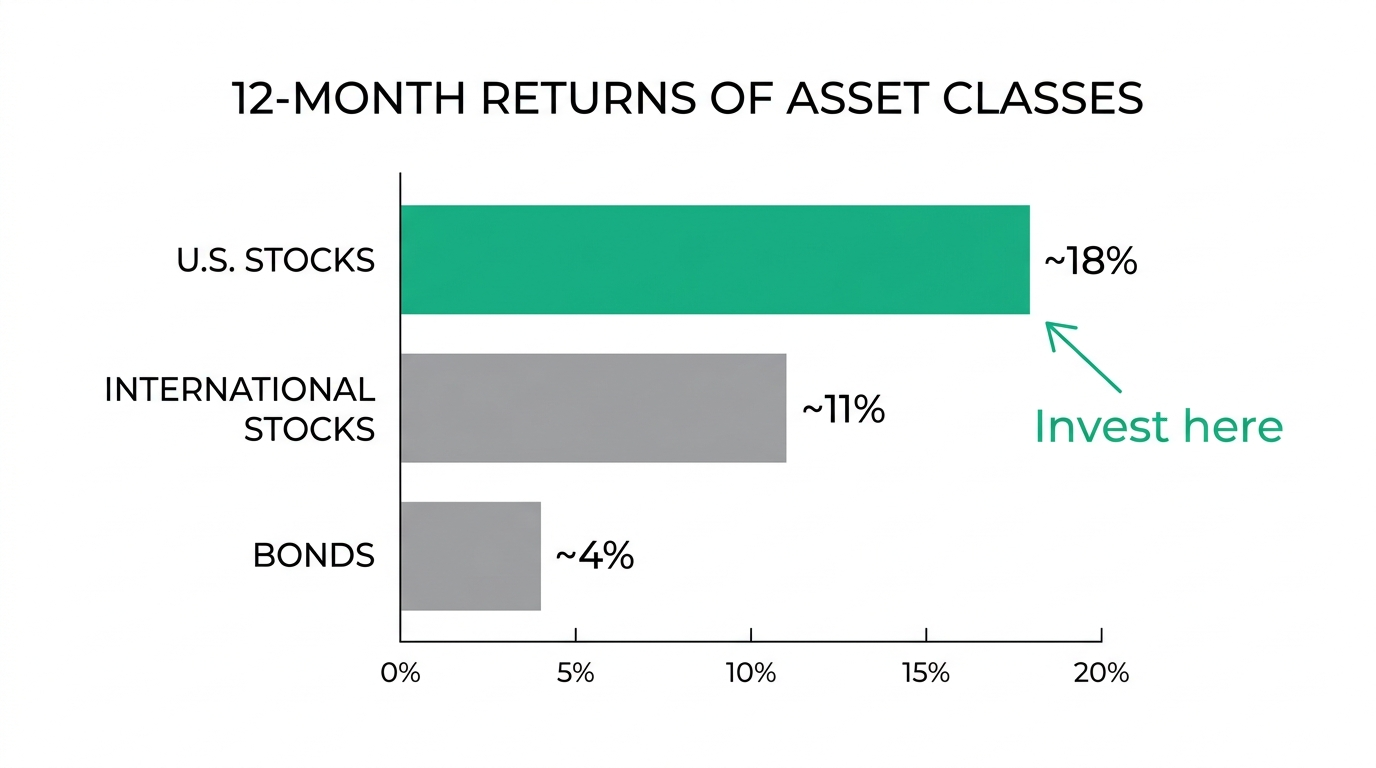

Relative momentum compares assets against each other rather than against a safe benchmark. You line up your options, say U.S. stocks, international stocks, and bonds, look at which one performed best over the past several months, and put your money there.

This is the original form of momentum that Jegadeesh and Titman documented in their 1993 study. They found that buying recent winners and selling recent losers produced significant excess returns over holding periods of 3 to 12 months. The finding has since been confirmed across most asset classes and geographic markets (Asness et al., 2013).

Relative momentum compares assets against each other rather than against a safe benchmark. You line up your options — say, U.S. stocks, international stocks, and bonds — look at which one has performed best over the past several months, and put your money there.

This is the original form of momentum that Jegadeesh and Titman documented in their landmark 1993 study. They found that buying recent winners and selling recent losers produced significant excess returns over holding periods of 3 to 12 months. This finding has since been confirmed across virtually every asset class and geographic market (Asness et al., 2013).

Relative momentum is good at optimizing returns during rising markets. It steers your portfolio toward the assets with the most strength, so you're riding the strongest wave.

Why You Need Both: The Missing Piece

Each type of momentum solves only half the problem. Used alone, each one has a blind spot.

Relative Momentum Alone: Great Picks, No Emergency Exit

If you only use relative momentum, you're always picking the best asset, but you're always invested. During a market crash, "the best asset" might just be the one falling the least. You're still losing money, just more slowly than everyone else.

Back to the horse race analogy: relative momentum picks the fastest horse, but what if the track is flooded? Picking the fastest horse doesn't help when none of them can run.

Absolute Momentum Alone: Good Defense, No Optimization

If you only use absolute momentum, you know when to get out, but when you're invested you don't know where to put your money. You might be holding an average asset when a much stronger option is available.

Combined: The Best of Both Worlds

When you combine both types, you get a complete system:

- Relative momentum tells you what to hold. It picks the strongest asset from your options.

- Absolute momentum tells you when to step aside. It moves you to safety when even the best option is trending down.

- Together, they capture gains in rising markets and limit damage in falling ones.

A Real Example: The 2008 Financial Crisis

Let's make this concrete with 2008.

In 2007, U.S. stocks were still doing reasonably well. A relative momentum strategy comparing U.S. stocks to international stocks would have been positioned in whichever market was strongest, rotating between the two based on performance. Everything looked fine.

Then 2008 hit. The S&P 500 fell roughly 37% that year. International stocks fell even harder: the MSCI World ex-U.S. dropped over 43%. A relative-only strategy would have been stuck. It might have correctly identified U.S. stocks as the "winner," but that winner was still collapsing. You'd still lose more than a third of your money.

Now imagine you also had an absolute momentum filter. By late 2007 or early 2008, the 12-month return of equities turned negative. They were trailing Treasury bills. The absolute signal would have triggered: move to safety. You'd have shifted into short-term bonds or cash while the storm raged.

As Antonacci (2013) showed in his research on risk premia harvesting, combining both signals would have avoided the worst of the 2008 drawdown while still capturing most of the gains during the recovery. The absolute filter didn't need to predict the crash. It simply reacted to the trend that had already started turning.

Gary Antonacci’s “Dual Momentum”: Putting It All Together

Gary Antonacci formalized this combination into a clear, actionable framework. In his 2014 book Dual Momentum Investing, he showed how to merge relative and absolute momentum into a single strategy simple enough for any investor to follow.

The basic logic:

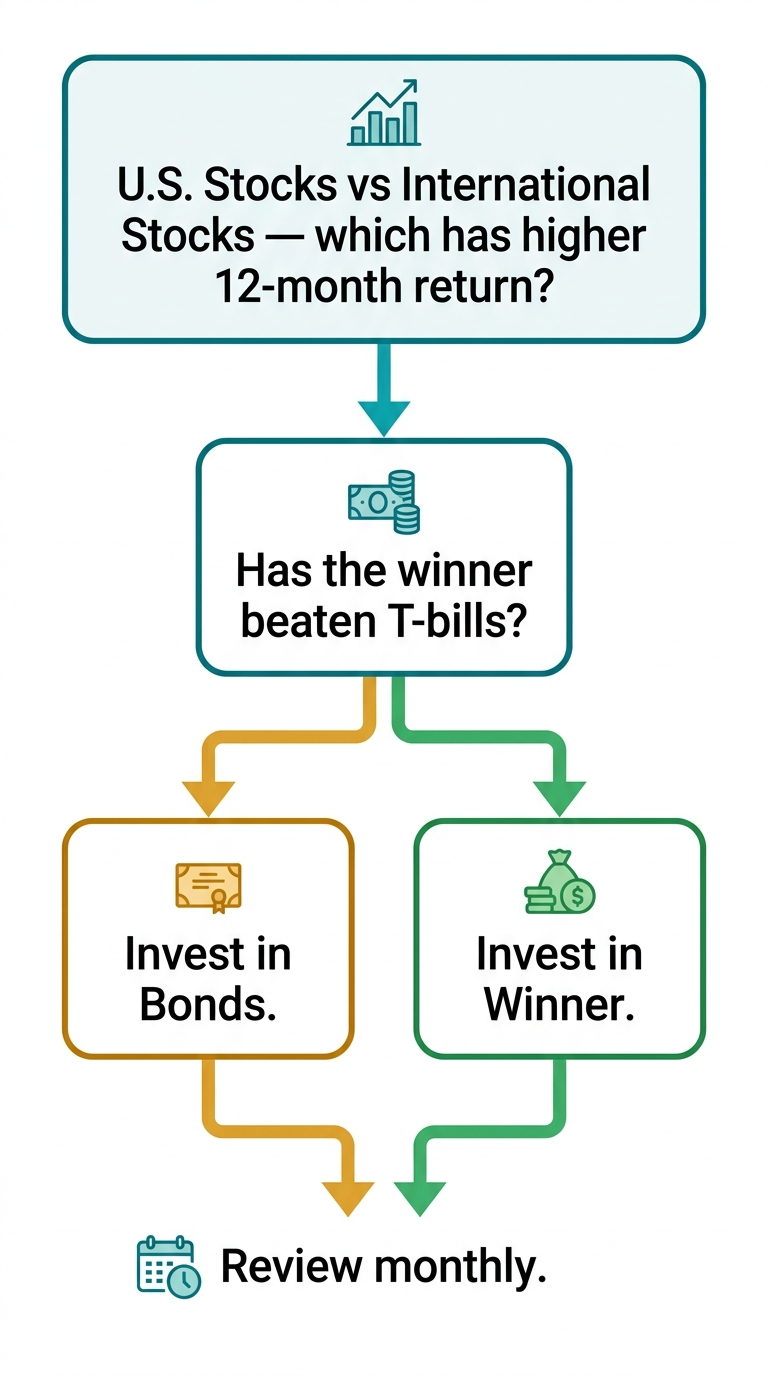

- Relative momentum: Compare U.S. stocks to international stocks. Whichever has a stronger 12-month return is the winner.

- Absolute momentum: Check if that winner has beaten Treasury bills over the same period. If yes, invest in it. If no, move to bonds.

- Repeat monthly: At the start of each month, run the same two checks and adjust if needed.

That's it. No complex math, no daily trading, no forecasting. Two questions, once a month.

Antonacci's backtesting showed that this dual approach delivered equity-like returns with smaller drawdowns during bear markets compared to buy-and-hold. His SSRN paper (Antonacci, 2013) provided the academic foundation, and the book (2014, chapters 4-6) laid out the practical implementation.

This Is the Foundation of Everything on reblnc.com

This matters because every strategy on reblnc.com is built on this dual momentum foundation. Whether we're looking at different asset classes, different lookback periods, or different rebalancing frequencies, the core logic is the same:

- Use relative momentum to pick the strongest assets.

- Use absolute momentum to confirm it's safe to invest.

- If the market is hostile, step aside and protect your capital.

The framework is well-supported by academic research, works across asset classes and geographies, and gives everyday investors a systematic way to manage risk without trying to predict the future.

Now that you understand both sides of momentum, the next articles will get practical: specific strategies, real portfolios, and how to put dual momentum to work with your own money.

Sources & Further Reading

- Antonacci, G. (2014). Dual Momentum Investing: An Innovative Strategy for Higher Returns with Lower Risk. McGraw-Hill Education. Chapters 4–6.

- Antonacci, G. (2013). “Risk Premia Harvesting Through Dual Momentum.” SSRN Working Paper. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2042750

- Moskowitz, T. J., Ooi, Y. H., & Pedersen, L. H. (2012). “Time Series Momentum.” Journal of Financial Economics, 104(2), 228–250.

- Jegadeesh, N. & Titman, S. (1993). “Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency.” The Journal of Finance, 48(1), 65–91.

- Asness, C. S., Moskowitz, T. J., & Pedersen, L. H. (2013). “Value and Momentum Everywhere.” The Journal of Finance, 68(3), 929–985.

Subscribe to our research

Get the latest tactical allocation strategies and academic whitepapers delivered to your inbox.